In this multi-part series I’m considering the many logistical challenges of the upcoming hydrogen economy. In Part 1 I considered the people necessary to start and sustain the hydrogen economy. In the subsequent parts/posts I’ll follow the hydrogen through the logistical supply chain to end use. This post is on hydrogen production. Transfer will be Part 3. End use will be Part 4.

Let me be up front that my expertise is hydrogen properties, storage, and distribution (i.e. logistics), and not production. Back in 2005 I saw everyone running into the production and power side (performance minded folks have a tendency towards power) and decided the logistics would quickly become the bottleneck for hydrogen. But the question of where all of the renewable energy will come from to produce the hydrogen the world needs must be addressed.

‘Water water everywhere and not a drop to drink’ & betting against the future

Hydrogen is the most abundant element in the universe at 74% of known mass (count % is even higher). 61% of the atoms in your body are hydrogen. 10.82% of the mass of Earth’s oceans is hydrogen. However, hydrogen is so reactive that it is seldom in pure form here on Earth. We’re literally in a sea of hydrogen, none of which is immediately available to us from an energy perspective. If we want pure hydrogen, we have to invest energy in some form to extract the hydrogen from host molecules. Once extracted, this highly valuable energy form, known as an energy vector or currency, can be used for many purposes.

Over the last year hydrogen has been in the world’s spotlight as a hope for avoiding climate catastrophe. Much of this excitement was generated by the IEA and a subsequent Bloomberg NEF team report, “New Energy Outlook 2020“. The later report estimates 100,000 TWh of renewable electricity production is needed to produce the green hydrogen necessary to provide 25% of the world’s energy required by 2050. That’s 6-8 times bigger than the world’s current electricity output and multiple industries are vying for that same share of increase. One of the Bloomberg NEF team members expressed skepticism to me because that increase will require a land mass roughly the size of India dedicated solely to renewable energy production. It’s tempting to look at the current state of the world and try to extrapolate to the future, but the future is always changing. What I’ve learned is to not get too carried away.

Michael Liebreich of the Bloomberg NEF team published a follow on report discussing the economics of this hydrogen production in the series, “Liebreich: Separating the hype from hydrogen – Part 1: The Supply Side.” Michael does an excellent job breaking down the associated costs of hydrogen production concluding “Will there be vast amounts of green hydrogen, cheaper than brown hydrogen by 2050? Absolutely,”.

So why write a piece on the logistics of green hydrogen production at all? Because the Liebreich report makes a classic mistake many, including Elon, make about predicting future technology scenarios. Any prediction of the future that says a technology will not be viable, without precluding the technology by the limits of physical law, is a speculative bet against the future.

Remember what I said above, the Leibreich report does an excellent job, my primary issue is this one sentence:

“It is also worth noting that green hydrogen based purely on offshore wind is unlikely to be competitive with production based on the combination of super-cheap solar and onshore wind.”

If we want to avert climate catastrophe, we need all the clean technologies working as well as possible. Statements like that put up blinders and cause researcher funding to be pulled, which risks holding back or even precluding a potential future that could go a long ways to helping humanity. If economics completely followed thermodynamics, and we awarded grants based on long term potential and progress and left popularity for business, this wouldn’t be an issue. So let’s do some quick calcs on just hydrogen production from off-shore wind here in the Pacific Northwest.

The potential of just one ‘unlikely’ approach

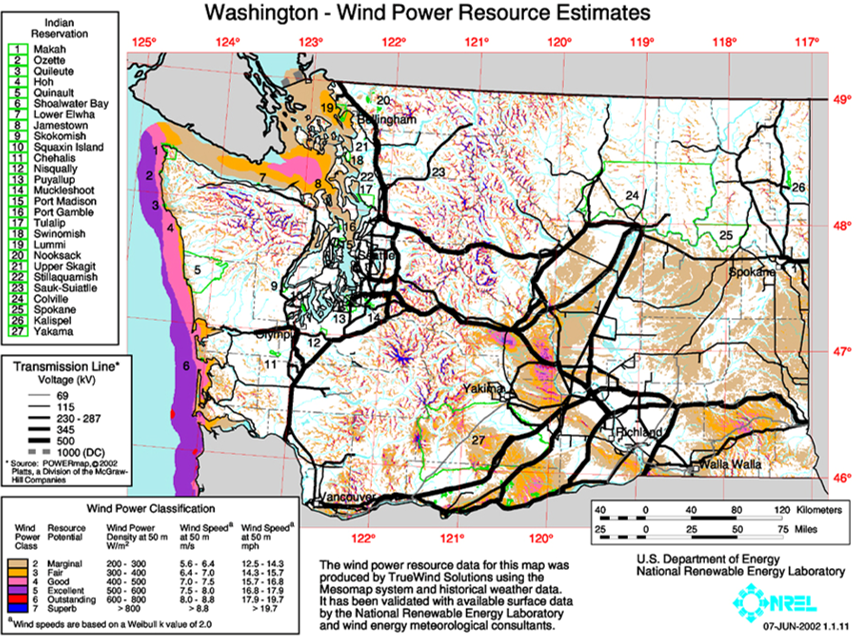

The following map shows the wind power resource estimates here in Washington state. What can be seen is that that the largest areas of ‘Excellent’ and ‘Outstanding’ wind resources, as measured by average speed and power density, are offshore. This is not where most of our current wind capacity is located and it should be noted that in 2015 roughly 7.1% of the state’s energy was generated from wind power. Since then the Bonneville Power Administration has removed on the order of 1 GW of installed wind capacity from it’s balancing authority due to the difficulties in regulating supply. These issues with regulation have been transferred to the utilities to encourage their own regulation. Many utilities immediately declared that Washington State has “too much wind power“. This shift is in part what prompted the Douglas County Public Utility District to install a Cummins 5 MW Proton Exchange Membrane (PEM) electrolyzer next to a hydroelectric dam. With requirements to meet the need to put wind on the grid, and water to flow through the dam, Douglas County PUD needed a scalable power regulation mechanism that they could control. The increased revenue potential of the resulting hydrogen was a big bonus.

We should expect to see many more utilities developing electrofuel projects in the region going forward as this is a way to increase both revenue generation and the percentage of installed renewables like wind and solar. Less than half of the permitted wind farms in the Columbia Gorge have been installed due to these wind intermittency issues that hydrogen could help to address. But to increase the total on-land capacity 6-8 times, as would be needed to address 25% of our energy demand from renewable hydrogen? We should keep all of our options on the table, including off-shore wind.

Washington State has the potential to produce at least 60.5 GW of offshore wind power after accounting for a 40% capacity factor based on a model from 2006 for 5 MW turbines. Just yesterday, Siemens Gamesa (the largest producer of offshore wind turbines) announced a new 14 MW turbine designed specifically for hydrogen production. I would be very interested to see these capacity factor models run again with these new 14 MW turbines. This off-shore wind resource will not create the regulation headaches for utilities caused by onshore wind.

But how much hydrogen could we produce with this 60.5 GW? This is enough energy to produce 22.1 million kilograms of hydrogen per day, assuming the 2006 numbers, the 141.9 MJ/kg higher heating value of hydrogen, and a 60% electrolyzer efficiency. WSU’s partner PNNL has produced catalysts capable of electrolyzing seawater.

How much hydrogen is that? Equivalent to ~2.5x our daily gasoline use in Washington State in 2018. Transportation accounts for 40% of Washington State’s CO2 emissions and this hydrogen could directly reduce or even eliminate this waste.

Serious Potential

The numbers, from just this one resource, indicate that green hydrogen has serious potential to reduce our reliance on fossil fuel imports and associated CO2 emissions in Washington State. There are many more potential generation sources in our state and many questions yet to be answered:

How will we store and transfer this hydrogen to the end users? That’s the next post.

What will the eventual costs be comparable to fossil fuels? Likely better before 2050.

What will the ecological impacts be if we eliminate our CO2 emissions, but create a field of eyesores off the coast? A 275 m tall turbine will still be visible up to 55 miles off the coast.

Regardless, it’s time for the State of Washington to do some hard thinking and number crunching about the serious potential for largescale hydrogen production. And, if we’re careful not to leave any viable options off the table, we’ll get to that clean future in 2050 we all want to see.